Are Pension Drawdown Calculators a Thing of the Past?

Quick history of how I stumbled upon Pension Drawdown Calculators A few years back, one of my close friends (let’s call him John) was inching

![]()

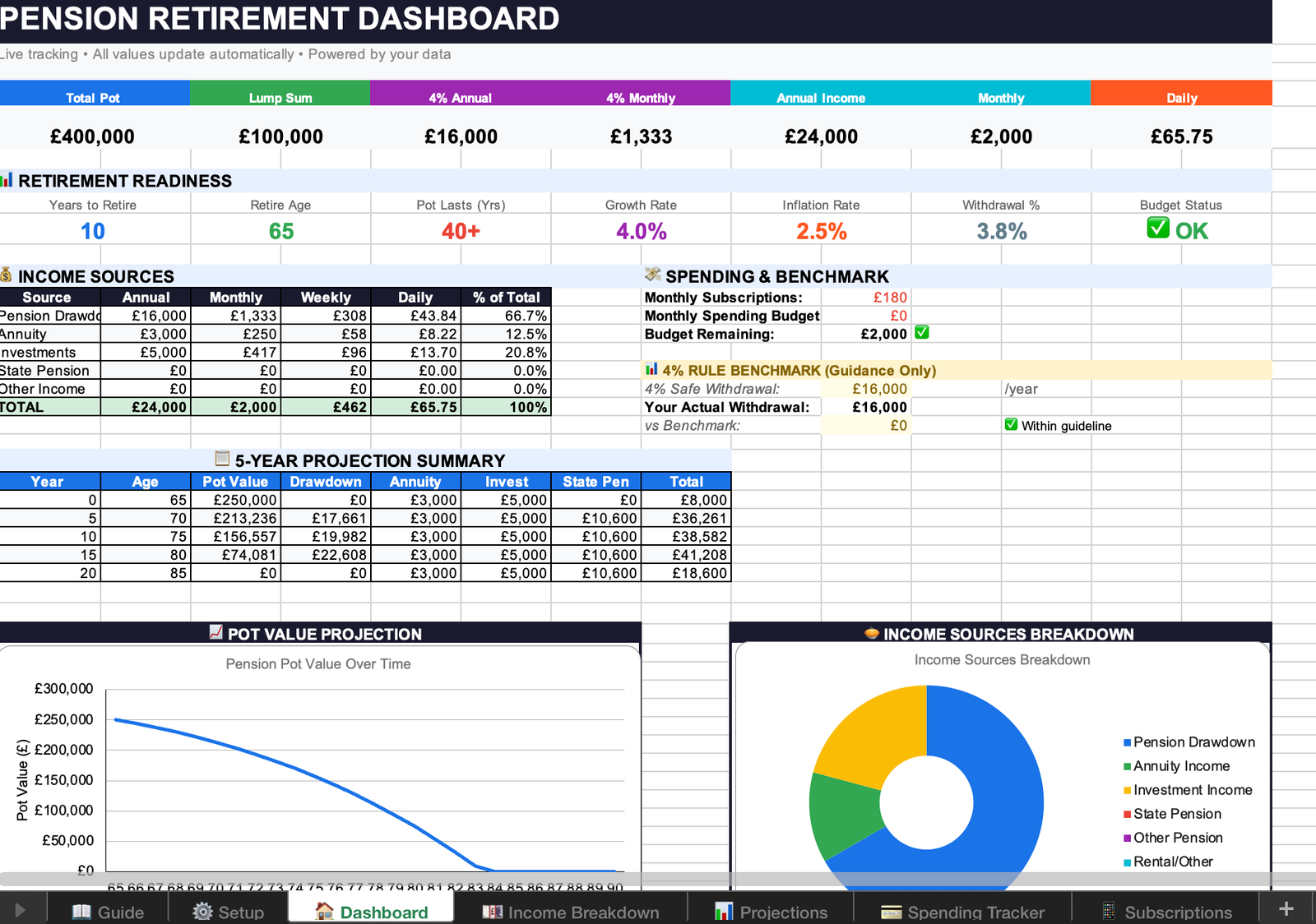

Enter your pension pot, choose a lump sum, set your ages, pick an annual withdrawal method, define leftover growth, and optionally buy an annuity or invest. We'll do the rest.